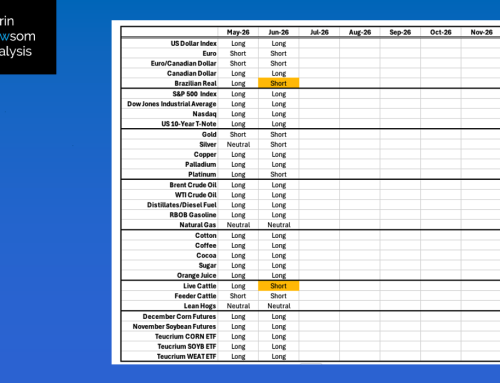

I pulled up the February Newsletter to do some research for this March piece, and before I could get into the meat of it I stopped at the opening: “January was quite a month. I won’t go so far as to call it “extraordinary” because much of what we saw has become “ordinary”.” The interesting thing is I could, and I guess I did, start this month’s Investment newsletter off with those same sentences. And when we recall February 2026, the Wheat sub-sector will quickly come to mind. Why? Because unlike the oilseed sub-sector, the three wheat markets were not driven by not necessarily the Truth Social media posts. When all was said and done, the three National Cash Indexes showed monthly gains of 22.99 cents (HRS), 29.39 cents (HRW), and 53.7 cents (SRW). As I said in Monthly Supply and Demand, I’m not convinced US wheat fundamentals changed as much as the Cash Indexes would indicate, putting a brighter spotlight on what happens over the course of the spring quarter (Q4).

In the latter part of February, a gentleman on the investment side of our business sent in some questions regarding the long-term potential of wheat in general, the HRW market in particular. I’m going to go over a few of his questions here, based on the old idea that if one person is wondering about something, others are likely as well.

Question 1) My friend started his email with, “HRW wheat may be breaking out from an extended consolidation period. Does your analysis suggest any investment possibilities in accumulating option LEAP calls in HRW wheat?

My Answer) Let me start by defining LEAP options. These are call (or put) options with expiration dates longer than nine months, and in the case of securities could be as much as three years. Given it was February 2026 (2/26), theoretically December calls could be viewed as LEAP options as November expiration was roughly 9 months out. As for my analysis, let’s look at the various factors:

- At the time, HRW market volatility was high. By the simplest metric, it is better to sell options when volatility is high, buy options when volatility is low. Volatility acts as multiplier of time value, and 9 months is a lot of time value to multiply meaning call options were likely overpriced. Additionally, the seasonal tendency for HRW volatility is to peak in the later March/early April timeframe meaning the position could be buying long-term options near the annual high in volatility.

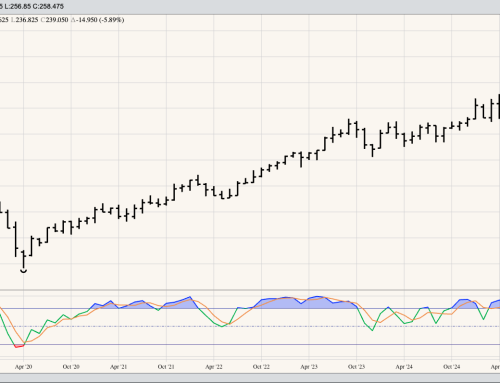

- The HRW market had moved into the upper percentages of its price distribution. Based on the charts Ben has built for Newsom Capital (slides 3 and 4), we can see HRW doesn’t spend much time at or above these price levels.

- Fundamentally the market was still bearish with both the July-September and September-December futures spread at or near bearish full commercial carry levels. The Dec-March spread was covering a neutral 50%, keeping in mind open interest is light that far out.

Question 2) If so, are there any particular months, years, or strike prices that have the greatest value and potential for price appreciation?

My Answer) First, you can tell the gentleman is looking at this from an investment point of view as he phrased the question in both terms used when evaluating potential in stocks: Value and Growth.

- From a value point of view, again based on the seasonally high market volatility, I think investments in options would be overpriced making it more difficult to return a long-term profit.

- As for growth, there is possibility, but I want to see the deferred spreads move closer to bullish levels of calculated full commercial carry, then look to see what long-term opportunities present themselves.

Question/Comment 3) I have considered the Teucrium Funds, but they are largely involved with futures and don’t perform well over longer time periods.

My thoughts) I agree, to a certain degree. He keeps a close eye on our investment Monthly Newsletter (Analysis and this Commentary) and was familiar with the Theoretical Position of buying Teucrium WEAT (or other Wheat related Exchanged Traded Funds (ETFs)) at the January settlement of $20.97. (For the record, WEAT closed February at $22.57 (slide 5), a monthly gain of $1.60 (7.6%)). The Teucrium WEAT fund is indeed based on futures, the SRW market to be exact, so wouldn’t necessarily move with HRW shorter term. Longer term, the three markets tend to move together. For a long-term investment, something along this line still seems to be a good opportunity, though I’m open to hearing discussions of other tools.

From a technical point of view, I like wheat as an investment. This fits with Rule #1: Don’t get crossways with the trend. From a fundamental point of view, I’m not convinced wheat has turned the corner from bearish to bullish. And as Rule #6 tells us, “Fundamentals win in the end”.

As always, thank you for your questions, comments, and conversations.

Darin Newsom