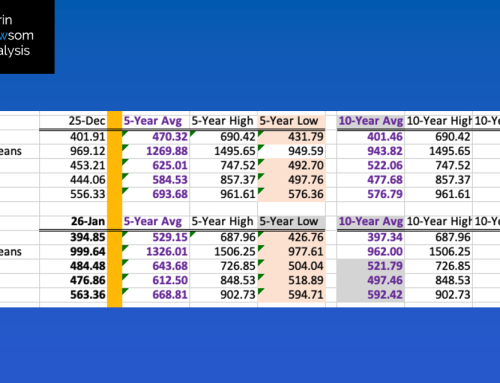

The bottom-line supply and demand number is stocks-to-use (s/u). I’ve long said stocks-to-use are the Readers’ Digest version of supply and demand, in that one number can tell us the bullishness, bearishness, or neutrality of a market’s fundamentals. I’ve also argued endlessly over the years with economists, with my point being there should be a direct correlation between stocks-to-use and cash price. Given my premise, I’ve developed my system between the two with all three major markets (wheat, corn, and soybeans) with the r-squared[i] at most 100% (all wheat) and at least 93% (soybeans). In all cases I’m using the cmdty National Cash Price Indexes, and in wheat that means HRW, SRW, and HRS have been weighted to reflect US production of all wheat supplies. The Darin Newsom Analysis, Inc. (DNAI) stocks-to-use numbers are calculated at the end of every month, and then compared to the previous month and the previous year. The DNAI numbers may not agree with subsequent USDA report estimates, but that is understandable given the DNAI numbers are real (based on national average cash prices) rather than imaginary (based on…I have no idea).

WHEAT: The 2021-2022 combined daily average cash price for the three major wheat markets was $6.90 at the end of September, correlating to a s/u figure of 26.6%. The end of August showed s/u of 27.5% and the previous September 47.5%. The key here is US wheat supply and demand continues to tighten, with futures spreads at the end of the month bullish (HRS, inverted), neutral-to-bullish (HRW), and neutral-to-bearish (SRW).

CORN: The 2021-2022 marketing year was only one month old at the end of September, and early harvest providing new supplies could be seen in the end of the month s/u calculation. The NCPI showed a daily average price during September of $5.12, correlating to s/u of 9.8%, slightly larger than the end of August 9.6% yet still well below the previous September figure of 12.8%. This was the first lower monthly price since September 2020, when the NCPI fell from $3.35 to $3.34, and again reflects early harvest pressure.

SOYBEANS: As with corn, the 2021-2022 soybean marketing year has just passed the one month stage with the daily average for the NSPI coming in at $12.37, down from the August figure of $12.83 that also gave us an ending s/u figure of 0.2%. This was the second tightest in history, trailing only the 0.1% calculated at the end of the 2013-2014 marketing year. And as I’ve said many times since this past Thursday, my end of the August calculation is why USDA’s stocks on hand as of September 1, the de facto ending stocks figure, of 256 mb is ludicrous. As for the end of September, the $12.37 correlates to s/u of 0.3%, still incredibly tight when compared to the previous September’s 5.0%.

[i] R-squared is defined as “a statistical measure of fit that indicates how much variation of a dependent variable is explained by the independent variable in a regression model.” (Investopedia). In my world, it is how closely related two (or more) variables are, in this case national average cash price and stocks-to-use.