Cash Corn: My Blink reaction (based on Malcolm Gladwell’s book “Blink”) is to say the cmdty National Corn Price Index (NCPI) remains in a major (long-term) downtrend. Activity during March, including a new high near $7.53, created a Wave B (second wave) peak of the major 3-wave downtrend pattern. By definition, depending on the type of Wave B taking place “the rally may test the old highs (forming a double top) or even exceed the old highs before turning back down.” (Technical Analysis of the Futures Market, John J. Murphy, 1986 ed., pg. 379) If this is indeed the case, then we would expect the NCPI to start working lower, eventually taking out the Wave A low near $4.86 from October 2021). This is the technical read. Fundamentally corn remains bullish, as indicated by inverted old-crop and new-crop futures spreads. While I’m wary of the technical pattern, Newsom’s Rule #6 says, “Fundamentals win in the end.”

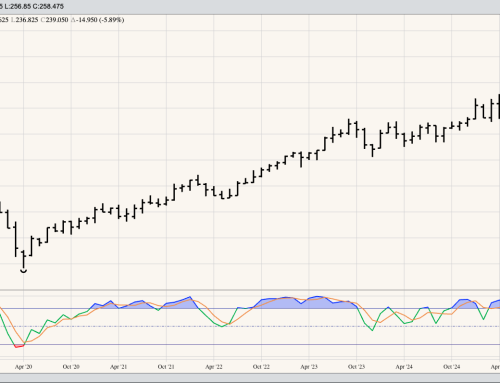

New-crop December Corn: The 2022 contract extended the major (long-term) uptrend on the Dec corn only continuous monthly chart to a high of $6.91 during March. From a technical point of view there could be almost $2.00 remaining in this move, with one set of pattern analysis putting a high-end target at $8.76. This would seem to be supported by bullish long-term fundamentals with the December contract gaining nearly 10 cents on July 2023 during March, the forward curve closing March at an inverse of 1.25 cents. Things could get interesting this spring and summer depending on weather, if US producers actually plant less than 90.0 million acres. On the bearish side, monthly stochastics are already well above the overbought level of 80% and could soon establish another bearish crossover.

Cash Soybeans: The cmdty National Soybean Price Index (NSPI) completed a bearish spike reversal during March. After rallying to a new high near $16.81 the NSPI closed near $16.65, down 23.0 cents for the month. This also looks to have completed a double top pattern, a normal characteristic of Wave B (see discussion in Cash Corn). It activity during March was a Wave B peak, Wave C would be expected to take out the Wave A low near $11.42 from November 2021. This is a possibility, over time, though the probability remains low given the strong inverse in the the soybean forward curve as far out as the 2023-2024 marketing year. If the US does start to see cancellations of rolling of old-crop export sales to new-crop, it could keep a lid on the NSPI while spring and summer weather moves the new-crop market.

New-crop November Soybeans: Despite the November 2022 contract posting a lower monthly close at the end of March, the major (long-term) trend still looks to be up. I’ve come to this conclusion based solely on the fact it has not completed a bearish reversal pattern. If November sees a couple months of consolidation, something that seems unlikely as we head into the volatile spring and summer seasons, it could eventually post a new 4-month low when/if the February low of $13.6225 becomes support. Monthly stochastics are indicating the contract should continue to fall, and we’ve already seen new-crop November had no problem falling $1.50 from its February high of $15.55. We need to be careful with new-crop soybeans, though also keeping in mind it the market remains long-term fundamentally bullish.