I’ve changed my monthly discussion of real month-end fundamentals for the various grain markets. I’m simplifying the conversation by applying the Law of Supply and Demand: Market Price is the point where the quantity demanded equals quantities available creating a market equilibrium. My take on this Law is tweaked by looking at “available supplies” rather than “total supplies”, an important distinction in the Grains sector given supplies can be held off the market in on-farm or commercial storage. If we consider the three variables in the equation (Market Price = Supply, Demand) the only one known is Market Price. Therefore, a study of Market Price is all that is needed to understand the relationship between the unknown variables of Supply and Demand.

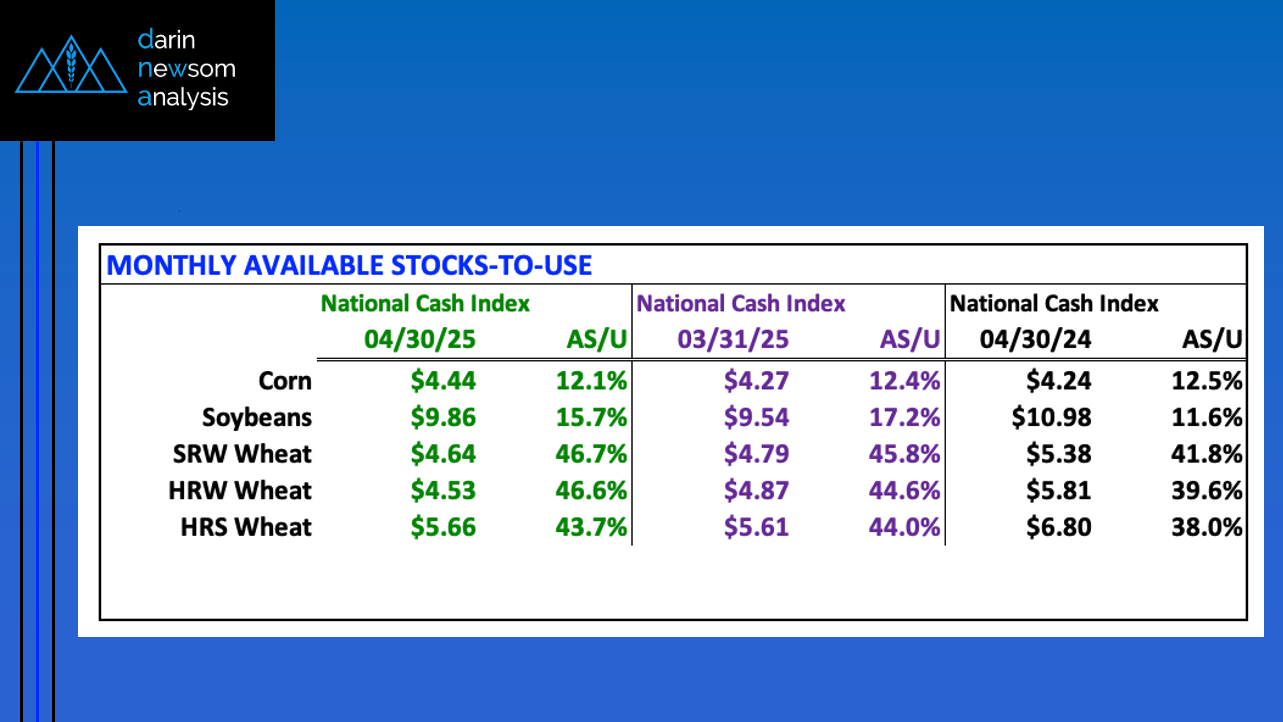

CORN: The National Corn Index (NCI) was calculated near $4.44 at the end of April, putting available stocks-to-use (as/u) at 12.1%. The end of March saw the NCI at $4.27 with as/u of 12.4% and April 2024 showed $4.24 and 12.5%. The US corn supply and demand tightened last month, not surprising from a seasonal standpoint as on-farm stored supplies move slower to off-farm storage during planting season. The end of April as/u was near but still slightly below the previous 10-year average April figure of 12.3%

SOYBEANS: The National Soybean Index (NSI) was calculated near $9.86 at the end of April, putting available stocks-to-use (as/u) at 15.7%. The end of March saw the NSI at $9.54 with as/u of 17.2% and April 2024 showed $10.98 and 11.6%. The US supply and demand tightened during April, an interesting development given all the outside noise in the market. Demand remains strong, though the US only shipped a reported 45 mb last month. During April 2024 the US shipped 61 mb. This tells us domestic crush demand continues to drive the US soybean market. The end of April as/u was still above the previous 10-year average April figure of 14.9%

SRW WHEAT: The National SRW Wheat Index (SWI) was calculated near $4.64 at the end of April, putting available stocks-to-use (as/u) at 46.7%. The end of March saw the SWI at $4.79 with as/u of 45.8% and April 2024 showed $5.38 and 41.8%. The 2025 as/u number was the largest April figure going back through 2020. The bottom line is the US SRW market remains fundamentally bearish with the next harvest drawing closer.

HRW WHEAT: The National HRW Wheat Index (HWI) was calculated near $4.53 at the end of April, putting available stocks-to-use (as/u) at 46.6%. The end of March saw the HWI at $4.87 with as/u of 44.6% and April 2024 showed $5.81 and 39.6%. The 2025 HRW as/u number was the largest April figure going back through 2020. The bottom line is the US HRW market remains fundamentally bearish heading toward the 2025 crop.

HRS WHEAT: The National HRS Wheat Index (HSI) was calculated near $5.66 at the end of April, putting available stocks-to-use (as/u) at 43.7%. The end of March saw the HSI at $5.61 with as/u of 44.0% and April 2024 showing $6.80 and 38.0%. The US HRS wheat supply and demand situation continued to tighten during April, albeit slightly. We need to keep in mind what I call the Wheat Reality*, not just in HRS but all wheat classes. The 2025 HRS as/u number was the second largest April figure going back through 2020. Given this, the bottom line is HRS wheat remains fundamentally bearish.

*The Wheat Reality tells us, “One bushel of wheat left over is too many.