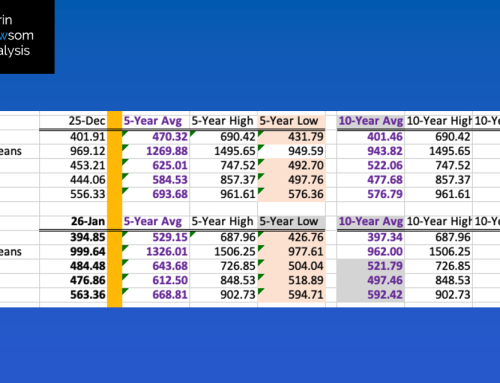

The bottom-line fundamental number is stocks-to-use. I’ve long said stocks-to-use is the Readers’ Digest version of supply and demand, in that this one number can tell us the bullishness, bearishness, or neutrality of a market’s fundamentals. I’ve also argued endlessly over the years with economists, my point being there should be a strong positive correlation between stocks-to-use and cash price. Given this premise, I’ve developed my system between the two for the five major markets (corn, soybeans, and three major wheat classes) with the r-squared[I]for all near 100%. Using this system I can pull data any day of the month, but by using the end of month number it gives us a picture of the available stocks-to-use (as/u) situation at month-end, a system that should smooth out the wide changes seen at the end of a marketing year. It also puts a spotlight on what I call the Marketing Year Misdirection, meaning supply and demand is a constant flow rather than a hard line drawn between old-crop and new-crop.

CORN: The national average cash price for corn was calculated at $5.31 on June 30, 2023, a price that correlates to an end of month available stocks-to-use (as/u) of 10.6%. The end of May showed $6.28 and 9.2% with last June coming in at $7.17 and 8.0%. The collapse during June, culminating with a 33.83-cent loss on Friday, June 30 indicates the 2022-2023 marketing year remains on the path laid out during the 2010-2011 to 2013-2014 time frame (four marketing years). This was the second possible scenario discussed last month, with a possible result the cash market not bottoming out until the summer of 2024. If this continues to be the case, then we would expect as/u to continue to grow and national average basis to consistently weaken.

SOYBEANS: The national average cash price for soybeans was calculated at $14,44 on June 30, 2023, a price that correlates to an end of month available stocks-to-use (as/u) of 4.5%. The end of May showed $12.74 and 7.2% with last June coming in at $15.86 and 3.0%. Despite the sharp gains by the cash index during June, particularly the 70.36 cents on Friday, June 30, I remain concerned about the technical picture of this fundamental read. As discussed the last couple months, the index’s monthly close-only chart continues to show a head and shoulder pattern. By definition, “a return move develops which is a bounce back to the bottom of the neckline…”. Given this, the rally by the cash index is not surprising, even discussed previously as a possibility, with the measured downside target still near $10.26 (bottom dashed red line).

HRW WHEAT: he national average cash price for HRW wheat was calculated at $7.53 on June 30, 2023, a price that correlates to an end of month available stocks-to-use (as/u) of 31.8%. The end of May showed $7.57 and 31.7% with last June coming in at $9.03 and 26.3%.What jumps out at me with the HRW cash index is it didn’t drop far during June despite harvest progressing and national average basis weakening as newly harvested bushels are sold. This again indicates a large part of the 2023 crop was damaged by drought across the US Southern Plains growing area.

SRW WHEAT: The national average cash price for SRW wheat was calculated at $5.97 on June 30, 2023, a price that correlates to an end of month available stocks-to-use (as/u) of 38.4%. The end of May showed $5.52 and 41.0% with last June coming in at $8.09 and 28.2%. The winter wheat situation gets even more interesting as the SRW cash index increased by 45 cents during June. This despite futures spreads growing more bearish, the the July-September covering 83% calculated full commercial carry at the close of Friday, June 30 and the September-December covering 69%, with 67% or more considered bearish.

HRS WHEAT: The national average cash price for HRS wheat was calculated at $7.75 on June 30, 2023, a price that correlates to an end of month available stocks-to-use (as/u) of 33.8%. The end of May showed $7.48 and 35.0% with last June coming in at $9.46 and 27.4%. The cash HRS index firmed during June indicating the supply and demand situation was tightening. Harvest remains a couple months away meaning merchandisers will have to continue to push for available supplies.

[i] R-squared is defined as “a statistical measure of fit that indicates how much variation of a dependent variable is explained by the independent variable in a regression model.” (Investopedia). In my world, it is how closely related two (or more) variables are, in this case national average cash price and stocks-to-use.