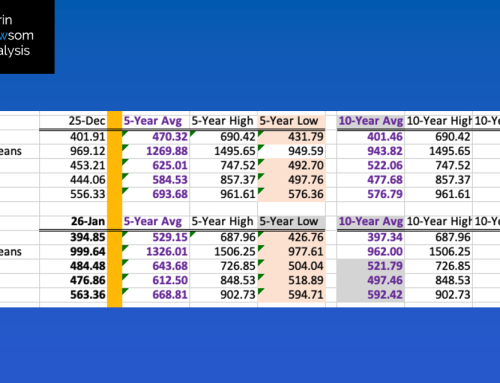

At the close of November, the daily average of the cmdty National Corn Price Index (NCPI, weighted national average cash price) for the 2020-2021 marketing year was calculated at $3.67. Based on my analysis back through the 2010-2011 marketing year, the $3.67 correlates to a continuous stocks-to-use calculation of 12.1%. Though only through Q1 of the 2020-2021 marketing year, if the NCBI stayed at this level it would be the tightest supply and demand situation since 2013-2014 when my calculation came in at 11.2% (green spotted market). Note this was the last marketing year when USDA underestimated US ending stocks-to-use, coming in at 9.2%. Both 2014-2015 and 2015-2016 (right hand side green markers, on correlation trendline) showed general agreement between my analysis of the NCBI and USDA with the last four marketing years (2016-2017 through 2019-2020) showing USDA with a systematic overestimation of ending stocks-to-use. Also note my analysis of the NCPI and stocks-to-use has a 99.5% correlation, again back through the 2010-2011 marketing year.

Some key factors through Q1:

- Supply

- The reality of tighter than reported supplies over the previous four marketing years has some home to roost

- National average basis continues to strengthen, with the cmdty National Corn Basis Index calculated at 13.5 cents under December futures ahead of the roll to the March issue.

- The NCBI started its journey with Dec 2020 at 35 cents under on September 1, 2020

- National average basis continues to strengthen, with the cmdty National Corn Basis Index calculated at 13.5 cents under December futures ahead of the roll to the March issue.

- The reality of tighter than reported supplies over the previous four marketing years has some home to roost

- Demand

- Feedyards continue to push the basis market as cattle on feed was reportedly 12 million head as of November 1, the second largest number on record.

- Reported export shipments, through Thursday, November 19 were 366.1 mb, a pace that projects total export shipments of 1.927 bb as compared to last marketing year’s reported shipments of 1.704 bb.

- Ethanol demand remains a huge question mark heading into 2020-2021 Q2