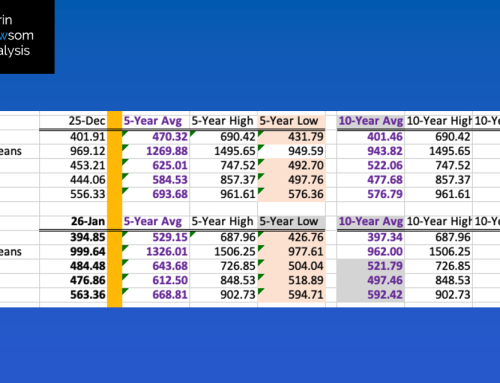

In its December round of Supply and Demand reports USDA estimated US ending stocks at 862 mb, down 15 mb from its November estimate. Total supplies were reduced by 5 mb due to a like cut in imports while demand was increased by 10 mb to 985 mb. As I talked about in Thursday morning’s Report Commentary looking at the latest weekly sales and shipment update, statistically the US is on pace to ship 1.026 bb. The combination of the 862 mb ending stocks estimate and new estimate of total demand of 2.112 bb puts USDA’s 2020-2021 ending stocks-to-use calculation at 40.8% (red column). Note this is down from USDA’s November calculation of 41.7% and my end of November calculation of 44.7% based on combined national average cash prices of HRW, SRW, and HRS using the respective cmdty National Wheat Price Indexes (weighted national average cash prices). The bottom line is USDA still looks to be underestimating US ending stocks despite its export estimate coming in below the latest pace projection for export demand. This continues to suggest USDA’s 2020-2021 beginning stocks of 1.028 bb (resulting in a Q4 ending stocks-to-use of 49.2%, green column) was too large, keeping in mind my final calculation was 45.8% and USDA’s own May ending stocks-to-use came in at 46%.