My monthly analysis of the key grain and oilseed markets will focus on the cmdty National Price Indexes (weighted national average cash prices). Recall from numerous previous discussions I view these as the intrinsic value of the individual markets meaning long-term monthly charts give us a good read on outlook.

At first glance, the monthly chart for the cmdty National SRW Wheat Price Index (SWPI) looks to be a jumbled mess. However, I still see the major (long-term) trend as down given the bearish spike reversal posted during May 2021. That being said, the SWPI then posted:

- A bullish spike reversal during June

- A bullish outside range during July

- A bearish spike reversal during August

- A bullish spike reversal during September

- and almost a new 4-month high during October, coming up fractions short of the August peak of $7.3162

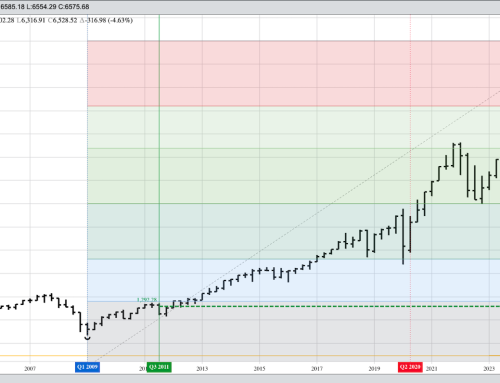

To clear things up a bit, I’ve applied the Wilhelmi Element (The only price that matters is the close) and attached a second chart, the SWPI monthly close only. Here the picture is much clearer, showing a continued major uptrend with a reversal being a monthly close below the previous 4-month mark of $6.5985. This fits with the general bullish US wheat fundamentals shown in my monthly stocks-to-use table (see Supply and Demand Commentary).